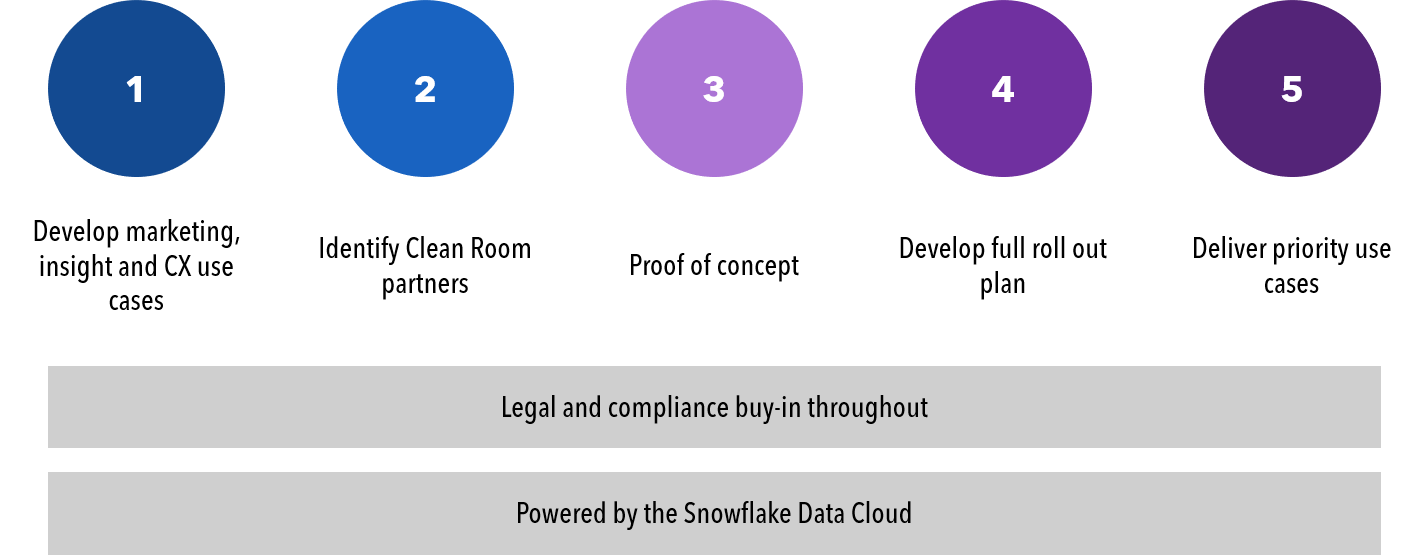

Posts A Customer Personalisation Platform to deliver change for financial services brands

A Customer Personalisation Platform to deliver change for financial services brands

Sagar Limbu

In this Article

Change within the financial services sector is complex. There are multiple stakeholders, regulatory needs, and often a base of legacy data and technology to unpick.

From our work with major brands, we know that the change is achievable and worthwhile. Investing in customer centricity will pay dividends in the long-term by reducing competitive threats, winning new customers, and ensuring retention of base customers.

To succeed in an increasingly competitive market, financial services brands need to establish change that encompasses:

A coherent data-driven strategy – where customer data is of a high quality and securely democratised to enable meaningful messaging to the individual

Establishing the right business targets and success measures – moving from short-term outcomes to long-term value for the customer and the organisation

A focus on your customers and the market context – understanding the needs and behaviours of both customers and prospects to better engage them

Maximising data and tech ROI – having the right tools to deliver the outcomes the business needs and then sweating the technology assets to deliver long-term ROI

Measure and optimise what matters – ensuring accurate reporting is fed through the business and that teams are empowered to act on those insights to optimise performance

Our challenge to leaders within financial services is to create a vision and become an agent of change. We want to work with brands who care about their customers and are making changes to show it. Therefore, our catalogue of services is developed to do amazing things with data and connect your brand with the individual.

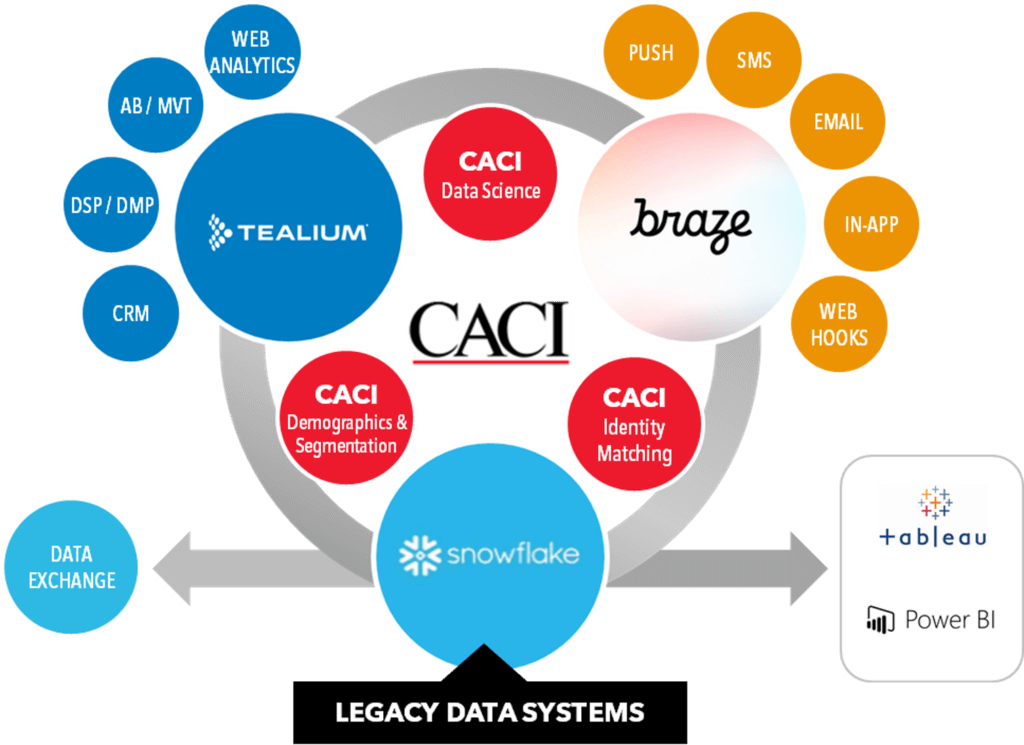

At CACI, we can improve marketing ROI through detailed attribution modelling. Our customer demographics and bespoke segmentations provide a more accurate profile of customer needs, market size, and even financial vulnerability. Technical decisions around investment in AI, decisioning or identity resolution are made by defining clear use cases for technology and designing future technical architectures.

This work led to CACI developing a framework for customer personalisation at scale. Working with leading vendors Tealium, Braze and Snowflake, we created a technology blueprint that can achieve full integration between enterprise data and the omnichannel experience.

To find out more about the CACI Customer Personalisation Platform or to discuss issues related to customer transformation, please get in touch.

You may also be interested in downloading this report which uncovers a surprising disconnect between what banks think and how customers feel about the customer experience, with statistics and insight gathered from 1,500 marketing leaders and 5,000 consumers.

You can also check out the previous parts of this blog series below:

Combining data and technology to deliver effective customer journeys in the financial services industry

Sagar Limbu

For many banks and building societies, legacy systems are a barrier for real-time, personalised customer engagement. Migrating experience platforms to a scalable, cloud-based platform, coupled with well-engineered decisioning, will enable banks and building societies to establish trust with consumers and subsequently maintain it.

The need for robust and reliable customer data

Banks and building societies are bound by financial services regulations to know the identity of their customers. Proper customer identification seeks to prevent criminal behaviour such as fraud, money laundering, or tax evasion. It is also a requirement for credit checks.

Having well-managed customer data enables lenders to identify the next best action for the customer, and create a customer strategy and journey tailored to each individual customer.

Inbound and outbound digital channels should be the ideal place to deliver these messages. But the use of digital technology is hampered by unfit processes and operating models that are combined with unscalable technology and batch processing.

With the right efforts to unlock the wealth of data held, the promise of real-time personalised messages that cut through the noise is very attainable for lenders.

Covid-19: a catalyst of change

The financial services sector responded quickly and earnestly to the challenges created by Covid-19. Payment holidays were offered, and staff were quickly relocated to home working setups to continue providing a good service.

The catalyst of change we all lived with created new levels of trust and empathy. This needs to be maintained by showing customers that the financial institutions really do care about them as individuals, especially in the current climate.

Mass mailings that push irrelevant products or services will erode that relationship. It shows a lack of care for the customer and a view of them as being a source of revenue and profit.

Making technology change last

To move forward, financial services marketers need to set a vision for the type of relationship they want to have with their customers.

This vision will determine the way that data is used, it will be at the heart of all campaigns and communications, it will alter working processes so that the organisation becomes more empathetic.

Through a clear and uniting vision, marketing technology will really be able to prove its value. Not just in delivering a better campaign, but by shaping the very experience and interaction an individual has with a brand. It will be about two-way interaction.

For useful input from over 200 financial services brands, 1,500 marketing leaders in the financial services industry and 5,000 financial services consumers, on how you should be evolving your customer marketing strategy to meet the needs of a changing consumer, download this recent report from CACI and Braze.

Check out the previous parts of this blog series below:

Last mile short cuts: the value of knowing your cost to serve

Sagar Limbu

Have you been hearing a lot about cost to serve lately? At the recent Last Mile – Leaders in Logistics event, it came up in practically every conversation we had with attendees and logistics experts.

If cost to serve is top of your agenda, we’d like to share some insights into how we calculate it and what you can do with the information. If it’s a relatively new concept to you, we plan to demystify and explain it in the following paragraphs.

Cost to serve is a valuable metric because it enables logistics operators to drive efficiency and support decision-making by understanding fulfilment costs across the entire supply chain.

Logistics operators and retailers are interested in the cost to serve for a range of different reasons. Depending on your organisation’s strategic priorities and current pressures, you might apply the insights to any of the following:

Reduce fuel costs and optimise your existing fleet

Transition and selection of electric vehicle (EV) fleets – ‘what-if?’ scenarios

Site selection, weighted by cost to serve

Sales forecast modelling, balanced by cost to serve

Scenario modelling, driven by cost to serve

There’s a relatively simple sum to calculate cost to serve: distance + fuel + time + environmental impact + resource. Measuring each element individually first, we look at the distance from distribution centre (DC) to store as well as from the store or distribution point to the end customer address. Fuel is costed according to delivery vehicle type. The time a delivery takes will take into account variable traffic and route conditions as well as accessibility on the doorstep. Emissions, noise and congestion add up to the environmental impact. And lastly, there’s the resource cost – including people, vehicles and equipment.

The sum might look fairly straightforward but gathering the data and putting it into comparable formats can be challenging. You may be familiar with data for distances, fuel consumption and resource costs, but tracking and estimating time to deliver can be more difficult, particularly in the last few metres when your driver is outside the vehicle.

Environmental impact is another measure that might be new to your business, but it’s increasingly important from a financial perspective as well as being a customer concern and area of corporate social responsibility. Emissions charging, tolls and vehicle tax all add cost into logistics and it’s important that they’re visible when it comes to planning and optimising services.

You can understand and tackle the most expensive cost to serve areas and apply best practice and understanding from areas with a lower cost to serve. It can help you prioritise future investment and reveal opportunities to streamline processes or boost training.

The logistics market can change fast – the recent fossil fuel price hikes were unexpected. Consumer preferences and competitor activity can affect your operation quickly. That’s why it’s not just a strategic measure: it’s important to monitor cost to serve continuously, so you can react quickly to emerging trends and keep control of costs throughout the supply chain.

CACI’s blend of logistics expertise and customer understanding can give you the edge when it comes to adding value and differentiating your services profitably. We can line up the data so you can measure your cost to serve accurately and keep your logistics operations delivering effectively, with a clear, business-wide understanding of costs and all the factors that affect the supply chain. Get in touch today at iwheeldon@caci.co.uk

Check out the other blogs in the Last mile short cuts series:

Three ways to stand out in a crowded insurance market

Sagar Limbu

In this Article

With new guidance in the FCA’s Consumer Duty directive, the financial services industry is being asked to get to know their customer better and meet their diverse needs. In a recent report produced by Braze & CACI, providing insight for financial services brands, it was found that 42% of EMEA consumers only use one financial services brand – so how can you retain their loyalty, trust and keep them engaged?

Technology innovation

The general insurance market has always been challenged with engagement, as the frequency of communication with its policy holders is low and concentrated at the point of policy inception, claim or renewal.

However, building trust is still crucial in this market.

Every insurer is now looking for new ways to harness technology for growth and competitive advantage. The use of AI and innovative tools is becoming more prevalent in the underwriting, claims and CRM process.

Harnessing your customer data through modern decisioning tools, and leveraging third-party demographic data to build a more holistic understanding of who your customer is, enables you to interject hyper personalised communications throughout the life of the policy, via the most appropriate channels, and actively give policy holders transparency over potential changes in premium.

Building trust

Whilst insurance may be seen as a “necessary purchase”, the payments aren’t usually greeted with good sentiment or the feeling of value for money.

However, the data and insights that much of this new technology generates creates the opportunity to engage policy holders more during the life of their policy.

For example, in car insurance, the use of telematics data could be used to talk to customers regularly about how they can improve their driving whilst reducing the cost at their next renewal. It’s well understood that people feel a sense of dread when a renewal comes around, fearing a policy price increase without a clear reason. As an insurer, why not reduce this surprise and help your customers maintain or reduce their premium?

If the data used to run the underwriting model changes, meaning that the car insurance policy may go up at renewal, it is better to let the customer know this early and explain why this has happened. This would increase trust and loyalty, reducing the likelihood that they might go to an aggregator when the renewal is due.

Even better, utilise predictive analytics to warn customers early of changes, enabling them to make changes in behaviour to help keep premiums down.

Understand your competition

The insurance market is made up of large general insurers through to niche specialists. Whilst brand reputation has a role to play, the heavy use of aggregators to seek out favourable deals is commonplace.

The opportunity is there for the more established brands to innovate and use their capability to invest in and truly leverage marketing technology and data to create a more trustworthy experience. For niche players, they can utilise their positioning to clearly communicate the benefits of their USP to customers.

With restrictions on the use of incentives for new consumers, all insurers need to consider other important elements of their offering and communicate this throughout the experience.

Throughout this blog series for the financial service industry, we break down the opportunities for marketers to build trust, loyalty and a superior customer experience with data and technology.

Last mile short cuts: the latest data-driven approaches to your biggest logistics challenges

Sagar Limbu

In this Article

Logistics data + customer understanding = optimal efficiency and competitiveness for logistics operators

That’s the first short cut we’d like to share with you in our series of concise last mile insights blogs. Inspired by our recent visit to the Last Mile – Leaders in Logistics event, we want to give you the lowdown on the latest proven techniques that can help you sharpen your efficiencies and improve your margins… and maybe transform your approach to some of the tough challenges that everyone in the sector is facing at the moment.

We had some great conversations at the Last Mile event, which helped us focus even harder on the key issues for sustained success and growth in logistics. Customer understanding and routing intelligence are key to effective planning for the last mile in a fast-changing, high-demand delivery market. Everyone wanted to talk about making the most of resources to match efficiency and cost management needs. Balancing this with customer expectations and the need for speed is a complex challenge.

Logistics organisations need to manage costs by adopting the most efficient service propositions. To identify these, they need to calculate demand accurately, for return logistics as well as deliveries. They need precision route planning solutions to help optimise routes and schedules, taking a data-driven approach to help them deploy the right fleet in the best way for different schedules.

Dealing well with change and variation is key in a high-volume consumer market. Predictive modelling helps organisations anticipate changes that will affect delivery schedules and customer requirements. Customers are constantly raising the bar on expectations of their home deliveries – they want the full range of pick-up options, availability of slots, fast same day or next day delivery and greener options.

Data is your not-so-secret weapon. Keep customers up to date with clear, proactive communication based on forward visibility from realistically planned schedules. Data modelling that reveals the ease or difficulty of accessing every property can inform realistic stop times and improve efficiency. Customer insight based on behavioural and demographic data helps you to create variable delivery cost models and fulfilment options to meet different situations and customer preferences.

Source: Statista, Online deliveries and returns in the United Kingdom (UK) 2022

To succeed and grow market share, logistics operators and the brands that use them need to deliver excellent customer experiences. With good historic and predictive data, you can be ready to meet ever more challenging delivery expectations and communicate positively with end customers. This can open the way to offering more green and sustainable services in a way that benefits customers, the environment and your bottom line.

The really big question is – how can your organisation do any of this in practice, in an affordable and low-risk way? In our coming blogs, we’ll zoom in on specific issues in a straightforward way. We’ll explain how we can help your logistics organisation optimise its approach to each challenge by using intelligence, data and tools in a smart and focused way.

With CACI’s logistics consultancy, you can make the unknown known, and own the future of your business. Get in touch today at iwheeldon@caci.co.uk

Look out for the next blogs in the Last mile short cuts series:

Creating human banking experiences through data-led marketing

Sagar Limbu

Our recent report, created in partnership with Braze, found that only 53% of financial services brands use advanced techniques like event-based and attribute-based personalisation when it comes to customer communications.

Using modern customer engagement technology will help financial services brands humanise the experience with their customers – as personalising each interaction using sophisticated decisioning algorithms will make the individual feel acknowledged. Real-time customer MarTech can manage two-way dialogue with customers, engaging them with the right content at the right time.

Great experiences start from the first contact

As the market grows ever more competitive and it becomes easier than ever to switch providers, creating the right first impression for your customers is essential.

It’s often thought that successful customer onboarding requires the customer to share a lot of data, but with the right customer strategy, marketing technology and third-party demographic data you can create an onboarding process that’s right for your customer without asking for more than your customer is willing to provide. Registration processes should be simple, not prohibitive to engagement, and show clear reasons for data collection. Consider neo-banks such as Plum who gamify their onboarding journey and make it simple to become a customer.

Collecting marketing consent is an often-neglected part of the sign-up process, with a series of check boxes tucked in at the end just before the terms and conditions acceptance. Improved consent processes are geared towards signing up for specific engaging content or benefits.

Education and transparency

Even though people are visiting branches less, it is still possible to create real trust through educating customers to support their decision making via your digital channels.

Many progressive banking and building society brands are now using interaction and behavioural data to point their customers to educational posts or feature tutorials. Brands can therefore help their customers to meet their individual goals, whether it’s to stay on budget, boost their credit scores, save for a new home, or other major life purchases.

Teaching customers to make the most of the digital tools available to them, and explaining how to achieve their financial goals, will demonstrate care and support. Additionally, being connected with the customer’s long-term ambitions means that bank and consumer are together for the same reason.

Humanising the experience

With Covid-19 accelerating the use of digital channels, the online experience needs to build trust by clearly acting in the customer’s best interests, like an in-branch customer service representative would.

Humanising the experience using empathy is key to this. Creating warmth and understanding around life events, in the same way a customer service representative would, is a powerful way to build that bond with your customer.

It’s critical that the customer journey promotes the value your brand brings by using every interaction, no matter the channel, to reinforce how each individual customer can financially better themselves.

Throughout this blog series for the financial service industry, we are breaking down the opportunities for marketers to create a personalised customer experience, and build brand loyalty through central decisioning engines, marketing attribution models, data modelling, machine learning and AI-driven recommendations. Continue reading at the links below:

For recent insights on how your customers feel about the experience they receive from their financial services providers, and for guidance on how you can better understand and meet shifting customer expectations, download our recent report – Banking on the Customer Journey.

How the banking and financial services sector can lean into a changing market

Sagar Limbu

In this Article

The evidence is clear, Covid-19 accelerated the pace of consumers’ changing behaviours.

Our analysis on consumer attitudes towards returning to branches highlighted a 32% reduction in bank branch visits post-covid, with even the most resistant to channel shift turning to apps and websites to manage their finances.

This is against a backdrop of other changes in the UK’s financial services sector that are impacting marketer’s abilities to connect with customers and prospects.

Retaining your savvy savers

Rising interest rates mean that people are becoming incentivised to both start saving again, and to switch savings accounts again, with savvy savers searching for the best deals.

Our recent consumer insights have found that the younger demographic are still expecting to save in the next 12 months. And it is to be expected that your competitors will increase their efforts to attract your savers to their products. You need to be ready to retain them!

Buoyant lending with a shift to the suburbs

Across the UK we saw a shift from the cities to the suburbs, driven by the opportunity to work from home more regularly. A reduced commute and a chance for more space was an opportunity many felt could not be missed.

Coupled with the government provocation of the housing policy, using changes to the stamp duty tax threshold, there has been an incredibly active homebuyer market.

However, recent economic factors have driven up the interest rates available on new mortgages and to those coming to the end of their fixed deals. Consumers are therefore incentivised more than ever to find the best available deal. This becomes a potential flash point for marketers who need to develop trust with customers so that the retention battle can be won.

Insurers need to rethink incentives

New legislation from the FCA means that insurers must be willing to offer the same incentive to new and renewing customers. Past use of aggressive incentives to win new customers’ needs to adapt to regulatory challenges.

Like the other macro conditions, this requires marketers to engage in longer-term marketing journeys with potential consumers, to win them and retain them with value driven propositions.

The need to communicate with the individual

Whichever way you cut it, there’s a lot of change to contend with for the financial services marketer.

From CACI’s perspective, we see there being winners and losers in the market across banking, lending and insurance.

The winners will be those who utilise data and technology to serve customers as individuals. To maintain engaged relationships based on trust and demonstrate how the brand is taking care of the financial interests of the individual.

Throughout our new blog series for the financial service industry (starting with this blog), we will break down the opportunities for marketers to address these challenges through central decisioning engines, marketing attribution models, data modelling, machine learning and AI-driven recommendations. Continue reading at the links below:

For insights on consumer attitudes towards their financial services provider’s marketing and communications, download this report, created by Braze in partnership with CACI. With input from over 200 financial services brands, 1,500 marketing leaders in the financial services industry and 5,000 financial services consumers, the report uncovers a surprising disconnect between what banks think and how customers feel. It also provides guidance for brands in the financial services industry to better understand and meet shifting customer expectations.

Marketing Measurement – a quick guide to getting it right!

Sagar Limbu

In this Article

We’ve all heard the well-worn clichés about the difficulty of measuring marketing effectiveness. As tired as they are, there are valid reasons for their persistence – determining what works, why, and who for can be complex. But does it have to be?

We still find that most organisations are relying on a ‘last click’ attribution approach to Digital & CRM measurement, and with good reason – most ‘off the shelf’ software platforms default to it, it is relatively easy to establish, and it can provide results, where previously there weren’t any! That said, it’s widely accepted that this lacks sophistication and accuracy, resulting in ‘best guess’ outputs that will over or understate the true impact of channel contribution.

So, how can you more accurately track the performance of your marketing, leaving you with actionable insights that can drive improved ROI?

Our tips for enhancing your marketing measurement

Moving to multi-touch attribution, considering all digital and direct channels, is typically the first step we recommend and is an area where we have had significant impact with clients. Having evaluated multiple approaches, we currently favour Markov Chain modelling, which calculates probabilities between successive channel interactions. This attributes impact to each channel, whilst also accounting for the sequencing of contacts between different channels.

Another approach we often recommend is to use Shapley Values to work out the ‘co-operation’ that can take place between channels. This can help us to calculate transition probabilities (to determine the paths taken between channels) and the impact of channels in combinations.

Once this level of capability and insight is established, we recommend that Channel Incrementality is established to further evidence the isolated contribution of each channel. This is achieved through a controlled testing approach, with channels stopped completely for short periods. We can advise on lean approaches here to minimise the time that channels are out of action.

In addition to the Attribution approach, we also find great value in also considering the impact of ATL channels and wider econometric factors. We have seen influences such as competitor activity, economic factors (such as cost of living & employment data), weather and global events (Covid & Brexit) all have a significant and measurable impact on sales. The key is to identify data that has significant variability (e.g., things that change regularly over time as anything too static can be all but impossible to infer impact from). Our recommended approach is to combine the Media Mix Modelling with Multi Touch Attribution to provide a true 360-degree view of performance.

This MMM approach is used to infer not only the size of the effect of each channel on sales, but also, where data permits, to determine the time decay of each channel – this defines the delay between any marketing channel activity, and its knock-on effect on sales. This may often differ significantly between channels. For these we typically apply bespoke Bayesian models which incorporate business knowledge to inform probabilities for any unknown parameters.

An additional approach we have seen add significant value is to consider ‘Segmented Attribution’ – moving from a channel or ‘overall marketing’ level focus, to a view of performance at the consumer segment level. This allows us to determine not only how effective a channel is, but also who it is effective for. This enables organisations to target the channel activity at the segments that will return the optimum engagement.

Finally, once all of this capability is established, we recommend that you not only use this to explain what has happened in the past, but also to create performance forecasts for future activity. Ongoing tracking and optimisation can keep this accurate as the business evolves, so that attribution becomes a key asset informing ongoing marketing decision-making and investment planning.

First launched on 10 March 1801, the UK census is a decennial questionnaire undertaken by the Office for National Statistics (ONS), National Records of Scotland (NRS) and Northern Ireland Statistics and Research Agency (NISRA) that asks a variety of demographic questions on age, sex, marital status, health, education, and housing.

The primary purpose of the UK census is to build a detailed snapshot of society at that current point in time. Helping national, regional, and local governments understand the people and households in their constituencies. This allows these government agencies to develop current policies or create new ones, as well as plan and fund services, including education, medical facilities such as doctor’s surgeries and hospitals, and transport infrastructures such as roads and new train routes.

The census is also used for other purposes, helping organisations and companies understand the society they interact with. This includes:

Academics and Education Institutions use census statistics to support research that they are working on.

Businesses using census information to help them understand their customers more effectively, i.e., a retail chain might use census population data to help decide where to open a new store.

How often is the UK Census, and when is the data released?

The responsibility for running the UK censuses is split between ONS, NRSand NIRSA based on their geographic region. The Office for National Statistics has overall responsibility for publishing census records and statistics for the whole of the UK.

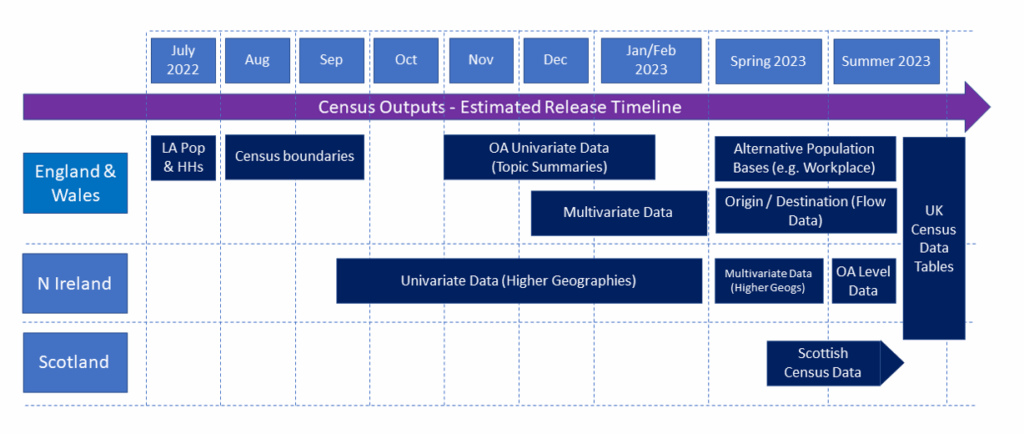

The data from the census is typically released in phases. For instance, in the first phase for England & Wales, local authority level population and household estimates were released, in June 2022. The three census offices each have their own timetable, with outputs staggered across a period of one to two years.

Because Scotland’s census took place a year after the rest of the UK, reference dates will differ. This will impact the comparability of UK census data, for this version.

Due to this, the three census offices are working closely to develop UK-wide census records, which involves consideration of how best to meet the challenges around comparability, coherence, timeliness, and accessibility of the information.

Below is an approximate timeline of the different subject releases based on the various census offices.

LA POP – Local Authority Population Data HH – Household Estimates OA – Output Area

CACI and the UK Census

The data from the UK census is used as input for many of CACI’s products, including Acorn, Ocean and Fresco. A wealth of companies uses these products, public sector bodies, charities, and not-for-profit organisations to help them understand their current customers, constituents, or beneficiaries more effectively, as well as market their products and services to like-minded individuals that fit the same demographic profile of their existing customers, saving them both expenditure and resource.

We also use the census as the baseline for CACI’s annual Up-to-Date Demographicsrelease, which providesthe latest estimates of key census variables (e.g. age, housing tenure, presence of children). These are modelled forward using various, more frequently updated data sources.

As the census is carried out only once every ten years, this provides an increasingly more reliable view of the population than the census data itself. Up-to-Date Demographics is available at census output area level.Consistent with this and for even more complex use cases, our annual Population and Household Estimates and Projections provide counts down to individual postcode levelsandproject forward for future years.

The first results of Census 2021 were published on Tuesday, 28 June 2022. These provided estimates of the number of people and households in England and Wales at local authority level. From this data, CACI was able to provide insight into the data to help:

The Ageing Population

The ageing population shown by this census follows our own predictions very closely, so it comes as no surprise. It does however throw up two significant questions.

Firstly, what does this mean for pensions? With proportionately fewer working people to retired people, will there be a greater emphasis on private pensions to cover the state shortfall?

And secondly, what does this mean for senior living facilities? We’ve recently been pushing the message that senior living needs to be looked at more rigorously in terms of its role within the wider housing stock and that all types need to be taken seriously.

The 2021 census only serves to vindicate that, and we would encourage local authorities and senior living developers or providers to engage with the data now to understand what their existing and future residents need, to ensure we have a fit-for-purpose housing mix for an ageing population.

Regional Growth and ‘Levelling Up’ –

It is great to see regions other than London taking the top spots in terms of population growth. It finds itself behind the East of England and South West, and in joint third place with the East Midlands, in terms of percentage increase.

More noticeable for their omission from the top of the charts are those regions further from London. Wales, the North East, and Yorkshire and The Humber are lagging behind quite significantly in terms of population growth, suggesting that the pull of living within reasonable commuting distance of London is still strong.

Salaries of course have a big role to play – the closer you are to London the higher both salary and disposable income tend to be. The growth we’re seeing in the census is more or less restricted to the southern part of England, so there is clearly a lot of work to be done with the ‘levelling up’ agenda, to entice people further away from the capital.

New release

On Wednesday, 2 November 2022, ONS also released their Demography and Migration Datafor England and Wales, their second release of Census 2021 data as part of their topic summaries.

This includes an update to population and household estimates for England and Wales, which now includes unrounded data by sex and single year of age, providing even more detail on individuals who were previously in age bands.

This meant that on Census Day, the size of the usual resident population in England and Wales was 59,597,542, which was the largest population ever recorded through a census in England and Wales. This meant that the population grew by more than 3.5 million (6.3%) since the last census in 2011 when it was 56,075,912.

It also contains information on household and resident characteristics, including household size, composition, deprivation status, and people’s marital and civil partnership status. Providing detailed insight into the makeup of the 24.8 million households across England and Wales. Such as although the number of households has increased to 24.8 million (up 6.1% from 23.4 million in 2011), the average household size in England and Wales in 2021 was 2.4 people per household, which is the same as in 2011.

Migration data is also included in this release providing further information on country of birth, passports held and year of arrival, helping us to understand internal and international population changes. For instance, of the 3.5 million (6.3%) increase in population from 2011 to 2021, 57.5% is positive net migration (the difference between those who immigrated into and emigrated out of England and Wales).

Understanding the impact of the cost of living in the water sector

Sagar Limbu

In this Article

The current impact of the cost of living crisis is being felt across the country. Being able to understand how these impacts are being felt across different customers groups and forecast future changes is imperative to creating a proactive customer support strategy. At CACI we have been researching and collating consumer insights and data on the cost of living to help you support your customers.

Some of the key insights we’ve seen from the research so far include:

Lower and middle affluent family groups are feeling the pressure the most

More than 2/3 of consumers have already started to change their behaviour by reducing their discretionary spend

Younger generations are more likely to turn to overdrafts and Buy Now Pay Later schemes to protect their social outgoings

Rising cost of energy bills has impacted all demographic groups, prompting high levels of concern ahead of the winter months

Economic uncertainty means 75% of consumers are worried about their own, their families, or other people’s finances

What does this mean for the water sector?

The water sector sits in a unique position with defined customer service areas that have a wide range of demographics, and a historically unengaged customer base resulting in a low awareness of support available for vulnerable customers.

CACI recently ran a roundtable to share key insights and discuss how the impact of the cost of living is being felt in the sector, and how water companies are looking to prepare for future forecasted impacts. The key outcomes from the session were:

Innovative partnerships provide new avenues – partnering with councils and landlords to identify and understand the set up for affordable housing allows support to be better directed to those that need it most.

Contact centres provide the first indication of change – whilst payment rates and direct debits currently remain strong after the summer months, the first sign of concern being seen is the increase in contact centre calls for help and support.

Clarity between water efficiency messaging and cost of living is needed – being able to identify the difference between a change in water use for environmental reasons vs to cap bills is key to ensuring the right messaging reaches the right customers.

Engaging the unengaged – is still a priority, in particular identifying those that qualify for social tariffs or support that aren’t currently using them.

Making insights actionable

Having the right data and customer understanding in place is key to enabling proactive communications, and to ensure the right support can be provided to customers. CACI’s data science team has created tools such as web-based water poverty tools, bespoke vulnerability indicators and forecasting tools to help you build proactive strategy with data driven insight.

As we continue to monitor the changing situation, sign up to our Cost of Living Podcast to get monthly updates.

Find out the full spectrum of work CACI does in the water sector from our Water Brochure.

For more detail on how CACI can support through enabling actionable insights, contact us here.

Supporting your Grocery Retail Strategies with Data Driven Intelligence

Sagar Limbu

In this Article

As with every industry Grocery Retail has had to adapt to a seismic shift in consumer attitudes and behaviour.

And those attitudes and behaviours continue to shift in response to local, national and even global events. The consumer has weathered the pandemic but is now staring down the challenges borne out of a cost of living crisis.

So, you need to make important decisions, and quickly. Flexibility is key. Having the data and tools at your disposal to make anything from adjustments that impact fine margins, right up to transformational change, is essential.

An innate understanding of your customer – their attitudes and behaviour – gives you the insight you need to attract new customers and retain existing ones. It’s also the foundation to building strong brand loyalty, even in challenging times.

CACI know more about your customers than anyone else. We combine a market leading demographic classification system with highly detailed footfall and spend data to provide you with everything you need to know about the way customers interact with your brand, your locations, and your competition.

Strategic decisions need strategic insight

CACI offer unrivalled insight into the fundamental relationship between people and place. Understanding this relationship speeds up decision-making and minimises risk from Cap Ex investment.

We are supporting grocery retailers with insight on:

The demographic profile of the catchment of each of your stores

The spend potential of the catchment in any location

The shifts in footfall and spend across times of day

The profiles of customers engaging with your competitors

Other locations similar to your best performing sites

Data driven network expansion driving the most ROI

Creating the right formats for the right locations to serve the local communities

MidCounties Co-operative

Unprecedented insight into the grocery retail market

Understanding the way customers interact with your brand, and how potential customers engage with your competition, is the first step to increasing your market share.

And with a complete view of the competitive landscape both nationally and locally, you will have the tools you need to develop strategies for success.

At a customer level you can:

Discover those that aren’t and why

Find out when they spend, how much they spend and what they spend their money on

Drive customer loyalty and win larger share of wallet

Identify highest spending customer groups and locate more of them

At a location level you can:

Benchmark locations against a national average across a range of criteria

Model catchment areas and market share catchments

Forecast how a particular location will change over time factoring demographic shift

Understand your local market share and competitor spend

Identify key growth opportunities in your store estate

Inform partnership strategy to generate greater footfall

Measure impact of your and competitor activity, e.g. marketing, store refurbs, etc

Sainsbury’s

The analysis to understand the digital / physical dynamic

The relationship between physical and digital has evolved, and demographics more inclined to visit a store are now comfortable online.

How has this affected your store network?

And how does online halo impact your performance across your physical store network?

Different demographics behave differently and will even favour different brands for different channels.

CACI can make sense of this and measure the success of each of your locations well beyond just what goes through the tills. Your best performing site might not be so obvious!

Optimising your store network with this analysis in your hands allows you to make the right decisions without negatively impacting on your multi-channel revenue lines. Future proof the business by effectively forecasting online as well as in store grocery demand.

Get in touch with us to show you how we do amazing things with data.

How wealth and asset managers should respond to the new FCA Consumer Duty

Sagar Limbu

In this Article

New plans from the Financial Conduct Authority (FCA) for increased consumer protection for financial services users, through a “fundamental shift in industry mindset” are to be confirmed by the end of July 2022.

The proposals include a new Consumer Principle that “a firm must act to deliver good outcomes for the retail consumers of its products”.

The regulator’s Consumer Duty directive is the latest in a series of measures tackling consumer needs in the financial services and wealth management sectors.

But how do the latest rules impact wealth and asset management firms? And how can a more effective use of data help firms increase customer knowledge and drive business growth, while ensuring compliance with the Consumer Duty?

How does the Consumer Duty impact wealth management firms?

Banks and building societies have moved steadily towards digitisation and customer-first policies over the past decade, but the wealth and asset management sector hasn’t moved as quickly.

While some firms have already adopted a business model that enables customer-led and technology-enabled strategy, it is only in the past 18 months that the importance of a data-led approach to wealth management has become prominent – and many firms are still playing catch-up. The Consumer Duty may well act as a catalyst for many to speed that change along.

The FCA is worried that, currently, financial services do not always work well for consumers, who are buying products and services that are not always fit for purpose, and not continuously receiving the best customer support.

Consumer Duty creates a shift towards making firms more proactive about the suitability of their products and services, to directly meet the needs of those they are sold to.

Wealth managers, along with other financial services firms, will need to improve consumer understanding, review the entire consumer lifecycle and journey, revisit how and what to include in customer marketing, and establish new ways to measure all these areas, in order to remain compliant.

“The new duty will drive a change in culture at firms. We expect firms to step up and put consumers at the heart of what they do, and we’ll be holding senior managers accountable if they do not.” warned Sheldon Mills, Executive Director of Consumer and Competition at the FCA.

Customer marketing – who are the new prospects?

Clearly, the FCA wants firms to better understand their customers. But how do wealth and asset managers do that? What steps do they need to take to make their business fit for purpose in a digital world and comply with Consumer Duty?

Regulatory pressure provides an opportunity to capture the market – collecting data and enriching it in order to tailor distribution and marketing.

Wealth managers are seeing changes in both customer behaviours and types of customers, and are moving away from the traditional investor to hunt out wealth in other areas – as they fight for market share. Meanwhile, fintech disruptors are raising the bar with innovative offerings.

Consumer insight is key. Young investors who are creating or inheriting their own wealth are increasingly important, as the older consumer market depletes. They are joined by more entry-level investors – and both personas have very strong customer service expectations.

These younger, and often more knowledgeable, investors are the customers of the future. They know they can invest quickly and easily online and they expect the same level of speed and ease of use in all their financial dealings.

A data-driven customer experience

Firms need to better understand the current and future needs of investors, those who might have a sophisticated, historic book of customers, now need to reach a broader audience – and CACI can help firms do that.

Consumer Duty firmly indicates products need to suit their customers, and firms need to be where investors can see them in order to market more broadly. Changing expectations might include more sustainable or green investments.

Those firms that recognise the need for better customer understanding are starting to bring in people with wider customer-first experience from other industries – increasing the sector’s pool of knowledge.

It is key to firms’ long-term growth that they do more with consolidated data – because if they don’t, they can be sure their competitors will. Firms will have data on customers, but many don’t know how to make the most of it.

At CACI we can help firms:

Understand their customers

Understand the market and identify opportunities

Know where potential and current customers are located, and their value

We can help brands across the wealth management, asset management and financial services space with demographic data and behavioural insights on investors.

Wealth and asset management firms looking to grow their business need to consider the importance of over- arching information and scalable transformation. Rich demographics on lifestyle, attitude and behaviours in the investment market, can empower better target distribution activity – driving revenue growth and increasing client engagement.

CACI will:

Provide detailed understanding of current investor behaviour needs and growth opportunities

Quantify the acquisition opportunity across regions to inform growth and investor engagement strategy

Enable optimisation of marketing performance across channels

Improve distribution performance through digital direct and intermediated channels

Demonstrate compliance with Consumer Duty to show that they are looking at, and understanding, customer needs

Or if you would like to find out more about how we can help, explore our services or get in touch.

Hybrid and online learning – putting perceptions in context

Sagar Limbu

For many universities, developing online technology used to be part of a three to five-year strategic plan to respond to modern learners’ needs. Students said they wanted more flexibility in how, when and where they study – virtual learning can provide this.

The pandemic forced universities to move forward quickly with these longer-term plans. The result was a rapid increase in digital resources and more collaboration with other institutions. This broke down location barriers and broadened reach.

Since the pandemic, not all universities have returned to face-to-face teaching across the board. This has sparked anger among many students, who feel they aren’t getting value for money.

For those that were able to access online learning, our study showed there was a strong sense that online tutorials and lectures could not replace the benefits of an in-person university education. Discussions were not as lively in tutor groups, lecturers were not inspiring, there was no sense of community as peers often turned off their cameras, and it was all too easy to step away from the screen. Now, looking back at their notes, students attribute gaps in their learning due to a lack of engagement.

Poor experiences in lockdown don’t mean digital learning is dead. There’s a big difference between the hastily reactive measures implemented in the pandemic and a well-informed, evidence-based, high quality hybrid learning strategy.

Universities are likely to continue delivering virtual materials as part of a hybrid delivery of education that maximises small interactive group learning and teaching in person but removes activities with less interaction, such as lectures. Our research with HEAT, Zero Gravity and students themselves suggests that – crucially – universities must take into account students’ background and experiences when designing hybrid programmes and resources.

OfS has set out guidelines and resources for learning institutions to help them set access and participation plans with commitments to address equality of opportunity. The open and free data they recommend is helpful, but we believe it’s insufficient. While IMD data is a recognised Government measure, it does not provide an up-to-date picture of deprivation. POLAR and IDACI measure attainment, but don’t explain what lies behind it.

Acorn and other commercial datasets provide vital demographic, lifestyle and behaviour insights that inform these baseline measures. It’s only by blending that universities can get the most from the OfS planning guidance to make informed decisions about how best to work with students.

Communication and consultation will be key. Students need to be convinced of the effectiveness and value of a hybrid model. They want their experiences in lockdown to be acknowledged and learned from. They want universities to share evidence that digital resources and teaching actively enhance student outcomes and are not just a way to reduce overheads or increase revenue from remote students.

In our recent paper, CACI’s University Data Team draws together student research, geodemographic data and expert opinion. It highlights priorities in the new post-pandemic world for outreach, admissions and widening participation (WP) leaders. Download the reportto find out how to build a successful WP strategy.

The bridge between Customer Experience and Brand

Sagar Limbu

It’s no surprise that customer experience has long been a priority for brands. There’s an overwhelming supply of research out there which demonstrates the importance and value of investing in CX; IBM found that businesses that prioritise CX see a 3x increase in their revenue.

However, one of the interesting differentiators between those who are really ‘winning’ in this space and those who are playing catch-up is the perception of the role of CX within brand development and communications. Whilst brand touchpoints are usually considered across ATL, TTL, BTL and POS, the reality is that brands are not just experienced within comms – they are engaged with across every touchpoint, platform or environment that a prospect or customer may find themselves in. A person should feel a seamless relationship with your brand, and with each interaction comes a wealth of information to harness and share within the business.

Where brands are losing out

Many businesses operate with marketing and customer experience departments that work independently of each other – the former focused on impressions and engagement metrics and the latter responsible for conversion optimisation and customer satisfaction. The gulf exists because these objectives are isolated, but both departments can offer invaluable information which supports the development of a cohesive customer and brand experience.

Demonstrating and measuring your values

Looking beyond customer experience ‘hygiene factors’ and conversion metrics allows you to build the right environment for your brand to flourish by having a bespoke approach to demonstrating your values. For an insurance brand, this could be the recognition and delivery of empathy and integrity when dealing with claims.

For an automotive brand this could be the sentiment of luxury and special attention that comes from purchasing an expensive new car. The whole brand falls down when these moments don’t live up to expectations, so these values should be present in all interactions, not just in communications.

Learning from the front line

Passing information back upstream is key to ensuring your brand is living up to the promise it sells. Customer reviews, call-centre recordings, satisfaction surveys, wait times and issue resolution rates are examples of information sources that would typically paint a picture of whether your brand is being perceived through the positive lens that is promised in communications.

Audiences will see straight through promises which are made but not kept to. Differentiating yourself in communications is only worthwhile if those differences are experienced when new customers (and existing ones) interact with you. If these are not present, audiences won’t stick around – they decided to give you a chance, so they can do the same for others just as quickly.

Operationally, your teams should be setup to interface and share regularly. Objectives and KPIs should straddle multiple teams and include metrics which govern your values, not just your bottom line.

Start bridging the gap

At CACI, we’re experienced in helping leading brands deliver a seamless customer experience. If you’re ready to start bridging the gap between your customer experience and brand but don’t know where to begin, our team of consultants can help you create a customer strategy and customer marketing solutions that deliver.

Responsible and sustainable practices

Sagar Limbu

In this Article

Could digitalisation save the planet?

Only if businesses can achieve sustainable cybersecurity and digital inclusion too

Digitalised businesses are onto a win-win – it’s good for corporate reputation, the planet and the environment to stop using paper and resource-consuming processes that create waste, take up storage space and hinder productivity. There are important caveats for doing all that good though: robust security for digital data and accessibility for all.

A well-understood approach to organisational corporate responsibility and sustainability is going paper-free and taking as many interactions and records as possible online. It avoids unnecessary worker travel and cuts the use of paper, postage, deliveries, physical storage and workspace, thereby reducing energy and fuel consumption.

Everyone knows the benefits of paperless offices

is “one of the most tangible examples of digitalization that has a positive impact on the environment while also providing major business performance benefits”. It estimates that even now, US businesses waste USD 8 billion on managing paper every year. It’s far more efficient and faster to transact, interact and work digitally.

Covid has accelerated adoption of these practices, as people have adapted rapidly to home-based and distanced working — which is one positive at least from the pandemic. But that means putting a lot more data online.

But hackers have an eye on the main chance. Since the pandemic, criminals have been quick to exploit security vulnerabilities created by a hasty shift to home-working and reactively moving transactional systems online. Recent headlines and share price drops show the impact of losing consumer and shareholder confidence for companies that experience data breaches and vulnerabilities.

Security by design is the gold standard for digitalisation

With so many financial transactions now executed digitally, security and trust are more important than ever to protect people’s money. Many consumers are far more aware and concerned about who is using their data and digital privacy. Building robust transactional apps, systems and data will continue to be crucial for success and reputation. Marketing compliance will need to be effective and transparent.

Security by design is the gold standard for planning, optimising and establishing cloud and digital infrastructure and systems. That means choosing and developing digital platforms and services in the specific context of cybersecurity – from thwarting hackers to back-up and recovery.

It also means that adopting new and more environmentally friendly technologies —from industrial plant equipment to electric cars, remote heating controls and contactless payments — must make digital security a top priority consideration. Hackers are not just delving into poorly password protected bank accounts for financial gain these days. They’re finding ways to hold organisations to ransom by infiltrating property, systems and infrastructure that are remotely and digitally controlled and operated.

On the surface, climate transformation has nothing to do with security. But dig a little deeper and you discover that it has profound implications indeed. The new technologies required for climate transformation will change both how businesses work and how they use technology. Security by design must be applied in order to prevent climate transformation becoming an excuse for greater vulnerability.

Smart organisations plan ahead and ask the right questions

Advanced digital mass security may not come cheap for larger organisations. It’s not just a one-off cost either: security protocols need to be maintained and measured against ISO 27001 and continually updated to mitigate the latest threats. But then there’s the potential risk and cost of neglecting security in any digitalisation solution. Smart businesses plan their budgets realistically and know that market-leading digital operations need to be underpinned by market-leading digital security.

Another important issue for ESG-aware organisations is the footprint of their digitalisation. The more data that’s online in the cloud, the more cloud storage is needed. Data warehouses have a big impact on the environment, not least because they consume so much electricity. Responsible businesses will ask questions of their cloud technology providers about their carbon offsetting and use of renewable energy sources, to maintain their integrity and reputation.

It’s not a good look to leave anyone behind

There’s another issue around digitalisation – and that’s digital inclusion. Consumers who are financially stretched typically don’t have such free access to the latest technology, devices and web access, which can lock them out of the digital environment, either partially or totally. Smartphones are increasingly the default device for managing banking and finances, but not everyone has one.

Income isn’t the only determinant of digital poverty. Location has an impact too: some rural areas struggle to access fast broadband, which can affect wealthier households. Some older citizens are digitally naïve. As well as struggling to access and use digital-only services, they may be more vulnerable to cyber-crime and scams. However good digitalisation may be for the wider environment, excluding less privileged demographics from online services and pricing generates damaging headlines and dissolves consumer loyalty and trust.

Consumer insight provides vital context for digital transformation

Savvy organisations seek insight to help them understand and avoid digital exclusion, using data like CACI’s Vulnerability Indicators. This includes detailed and granular digital vulnerability data that allows organisations to identify people who lack digital knowledge or may have little or no access to technology and the web.

Assessing and planning to enable digital inclusion must be a priority aspect of digitalisation programmes and initiatives. Responsible brands and public organisations need to understand the impact on their entire audience before assuming that the best choice is to move everything online, without exception.

Digitalisation is the right thing to do for the planet – as long as we do it right

There are huge gains to be made for our planet by embracing digitalization, cutting our consumption of the planet’s physical resources and improving efficiency and energy use in everyday life. But organisations must do this in well-considered way, taking into account the new risks and challenges that a fully digital world presents.

To maintain their integrity and reputation, businesses also need to consult and consider their customers and audiences and help them with digital adoption, as well as scrutinising and challenging the environmental practices of their own digital service providers.

If you’d like to know more about optimising processes and energy efficiency through data science or developing waste-reducing digital services and tools that meet current consumer needs, talk to the experts at CACI.

Consumer demand for more sustainable consumer transport is high and market conditions support mainstream EV adoption. What do motor brands, consumer destinations and logistics operators need to know, to make the most of this electrifying opportunity?

In our fourth blog in a regular series focusing on environmental, social and governance (ESG), our focus is on electric vehicles – an increasingly common sight on the UK’s roads.

These days it’s not just celebs and influencers who parade their green credentials with their Prius or Tesla. More choice, better charging infrastructure, longer vehicle ranges, affordable finance and fiscal incentives are persuading more and more ordinary consumers to join the EV gang.

Scenes of panic over presumed fuel shortages in autumn 2021 put the growing number of electric vehicle (EV) owners in a strong position. Suddenly, everyone wanted one – showrooms were inundated with enquiries and prospective owners joined waiting lists for test drives and for the privilege of buying new vehicles.

It feels like we’re now at the point of mass adoption, with the 2030 ban on new fossil fuel vehicle sales less than a decade away. Manufacturers, dealerships, fleet operators, drivers and infrastructure owners are all adapting fast to the changing market – what does the future hold and how can data insight help everyone thrive?

Who’s buying EVs?

Government and industry initiatives designed to accelerate EV adoption need to understand differences in consumer opinions and propensity to buy EVs. CACI’s 2021 EV survey shows that age and affluence both influence consumer behaviour – even when they have the means to buy an EV, older consumers are less keen. They tend to be concerned about range, despite typically making shorter journeys. That insight can help to explore the inhibitors and shape messaging to overcome consumer concerns.

We also identified less known benefits that could make EVs more attractive if consumers knew about them.

That suggests there’s an opportunity to tell consumers what they could save beyond the obvious cost of refuelling.

Data and insight are invaluable to manufacturers who need to know who to target, both in the way they design new vehicles and the way they promote them. New brands have risen rapidly to take advantage of the global opportunity for more sustainable consumer travel. Few UK consumers had heard of Polestar three years ago – now their cars are a common sight and the brand is well known from TV and digital advertising.

We’ve worked with Mazda to help them tailor content and produce engaging campaigns that appeal to the best audiences for their MX-30 EV. Current, accurate consumer data and granular analytics are key to the “impressive” results Mazda has achieved.

Is the infrastructure keeping pace?

Service stations, retail operators and landlords need to understand the opportunity so they can make the business case to invest in charging points. They need to drill into consumer and market data for EV adoption and understand the impact on their core users and customers.

If these organisations can’t size the demand and provide suitable charging facilities, they risk losing customers to better equipped rival sites. As well as losing revenue, that could depreciate real estate assets. In our EV survey, 55% of respondents said they would be influenced to visit a specific location if it provided an EV charging point.

Energy providers also rely on insight into consumer patterns of EV adoption, so they can plan infrastructure and provision. We’ve recently worked with EDF Energy to help them plan for demand and promote their home charging tariffs. A series of highly targeted campaigns engaged customers who already own or were at the point of purchasing an EV, to provide timely and relevant info and offers.

Have EVs lived up to their promise for early adopters?

Our survey showed that improved range in the latest EVs has supported strong owner satisfaction. As early adopters trade in and trade up, there will be more second-hand vehicles available, allowing more consumers to adopt EVs. EV ownership will be mainstream rather than a novel talking point.

There’s an opportunity for EV brands to focus on the capabilities of the latest EVs, to create a tipping point for hesitant or sceptical prospects.

How much does sustainability really matter to purchasers?

Blanket news coverage around COP-26 has increased public awareness and concern about sustainability still further. This impetus nudges more consumers to look beyond their initial perceptions of EVs, because they want to do their bit for the environment.

Consumer concern has a knock-on effect for the brands and service providers they use. Fleet and logistics operators are responding to growing awareness of the environmental damage from diesel van pollution. Consumers aren’t turning away from home deliveries, but they do want to see more sustainable approaches. Fleet and light commercial vehicles are swelling the EV market. Motor industry body the SMMT shared a recent survey that suggests fleet operators could collectively reduce CO2 emissions by almost a third through a switch to EVs.

What’s next for EV brands and related commercial and consumer sectors?

The EV market is relatively new and very fast-growing. Consumer desire, mainstream infrastructure, government legislation and attractive savings are creating a perfect storm of opportunity for EV brands. Data about customer perceptions and needs is vital for competitive advantage.

Meanwhile, many other sectors need insight into who’s driving what and where, so they can adapt facilities and propositions to make the most of the opportunity. European and global brands and businesses must seek local data, because every market is different.

Despite entreaties to use more public transport, UK consumers love the convenience of their own private vehicles. And for many, the Covid pandemic has made cars feel like a safer option. Responsible EV messaging as well as smart product development and marketing can help take carbon emissions from private and commercial vehicles off our roads and out of city centres.

We anticipate that consumers will want more and more in terms of green accountability from brands and fleet operators – such as understanding the full carbon footprint of manufacture and delivery. They’ll evolve their opinions as their own experience expands. Keeping pace with these expectations and behaviours through reliable and up-to-date consumer insight is key to commanding market share.

If you’d like to know more about acquiring consumer data that can keep your organisation ahead of EV trends and markets in the UK and beyond, talk to our sustainability insight experts at CACI.

CACI’s ESG Score can help you identify which ESG factors are most important to your customers. Download our product sheet to find out more.

Technology helps reduce waste for consumers and businesses

Sagar Limbu

In this Article

There’s a long way to go, but innovative technology is proving key to tackling waste on the global scale needed to protect our planet.

Waste doesn’t just mean physical deposits into landfill. It’s also about overconsumption and excess, from squandering energy or making unnecessary journeys to wasting water or making needless purchases, even if they are supposedly environmentally friendly. Environmental campaigners promote the mantra ‘reduce, reuse, recycle’ – if you can avoid demanding, producing and discarding an item in the first place, that means there’s less need to resort to recycling as a third best option.

The will to reduce waste is there and growing among consumers. But they need easy and affordable ways to choose low-waste lifestyles and products. Businesses, governments and service providers are stepping up to the challenge of becoming more efficient and sustainable to enable large-scale change. Everyone’s looking to technology for ground-breaking, digitally enabled approaches to waste reduction.

Convenience is key for consumers to prioritise waste reduction

Phone apps can help consumers to manage their waste. Waste processors like re3 have developed apps that provide information about recycling facilities and let people book visits to recycling centres. Local authorities have developed app-based incentives: in Nottingham, residents can earn points and prizes through the Green Rewards scheme by reducing waste with simple actions, from turning off lights to using public transport or recycling responsibly.

Capsule coffee machine owners can arrange free recycling collections for their used capsules through apps or on websites, making it easy to return rather than binning old capsules from brands including Nespresso and Dolce Gousto.

These are encouraging schemes that help avoid waste going into landfill. But there’s scope to use apps and consumer tech to prevent the creation of waste in the first place. The Scrapp app goes further, giving consumers information about the CO2 they save with each responsible recycling action and helping them reduce waste by understanding the carbon footprint of household items, so they can choose better to waste less of the planet’s resources. It also offers a reward scheme.

Apps help promote reuse as well as recycling

Using more reusable containers within a genuine circular economy, rather than recyclable ones, would cut down on production. Supermarket deliveries might arrive in sturdy bags or crates that consumers would retain until the next visit or drop off at a collection point. Applying tracker device technologies (similar to the Tile or AirTag) could make this viable, avoiding loss and theft and making sure customer deposits were refunded accurately and promptly.

The UK recycling rate for waste from households was 46.2% in 2019

Better planning and analytics help transport organisations cut fuel waste

Commercially and on a much larger scale, technology solutions are helping businesses reduce their consumption of resources, from designing products to use fewer raw materials to cutting down on the energy needed for operations and services.

CACI’s Real-Time Airport system is helping customers in the aviation sector reduce fuel usage. By optimising aircraft movements through algorithms and analytics, Heathrow airport can delay planes starting their engines and cut down on the time they spend queuing before take-off with the engines running.

This has created a massive 10% overall reduction in taxi times at Heathrow – that’s a significant benefit to the environment through reduced fuel burn as well as a better experience for air passengers.

Data modelling can make waste reduction a key factor in overall strategy

Increasingly, organisations will use advanced modelling and simulation to understand the impact of their actions on waste generation. Building in energy and carbon consumption to business models means that companies can shape their strategy and prioritise their activities to minimise waste.

Rapidly evolving artificial intelligence and machine learning capabilities can process more and more detailed and subtle information and show in depth the full range of consequences both for waste generation and wasteful use of resources. Companies can promote their low-waste approaches to customers and show the evidence behind their choices. It’s a more innovative and proactive approach to doing things very differently, rather than trying to reform old, wasteful ways of operating.

Digital convenience is key to influencing behaviour and sharing information

Apps, devices and websites use the power of digital media to raise the profile of waste-reduction and nudge consumers into making better choices. Apps like Nest provide information about heating costs and energy consumption then optimise energy usage throughout the day, cutting down on waste in gas and electricity. Utilities companies provide and connect digital smart meters, giving consumers real-time information on resource consumption so they have the power to change their habits to reduce bills and therefore usage.

Community websites and apps (such as Freecycle and Freegle) for passing on consumer goods and appliances locally give consumers a quick way to get rid of unwanted items or meet a need without buying new.

Private messaging protects privacy and means people don’t have to share their address until they’re sure the other person is genuine.

Carrie Johnson and other celebrities have raised the profile of fashion hire through platforms like My Wardrobe HQ, making it cool to rent an outfit for a smart occasion rather than buying new and discarding outfits after one or two wears. High quality digital photography and easy booking through online apps create a frictionless experience that high-end consumers are willing to embrace.

Using fuel more wisely and optimising electric vehicle transit

In travel and transport, ridesharing and public transport e-ticketing and information apps make it easier for customers to travel conveniently without needing to run their own vehicle, cutting down on private fuel usage.

Home delivery services operated on fast and efficient digital platforms cut down on individual journeys to the shops. But they have driven an explosion in courier and commercial delivery services, adding to urban congestion. Leading delivery networks already use logistics technology and data to optimise the efficiency of their delivery fleets, selecting the best routes and delivery sequences to cut down on fuel usage. As electric vehicles become more commonplace, adaptive software is key to planning routes that factor in battery life and charging times.

Reduce and re-use first and second

Recycling is good, but reducing and reusing are better, when it comes to waste reduction. Consumers and businesses are both tapping into the power of digital apps and data analytics to inform themselves and adopt new approaches that cut consumption of goods and resources.

Already, organisations can achieve substantial reductions in energy consumption and wasted materials by optimising their processes and harnessing technology to eliminate inefficiencies across their operations. Digital innovation makes it possible to combine this approach with user-friendly apps and websites, so it’s easier for customers to understand the impact of their choices and to consume and waste less.

If you’d like to know more about optimising processes and energy efficiency through data science or developing waste-reducing digital services and tools that meet current consumer needs, talk to the experts at CACI.

Understanding which ESG factors are most important to your customer is fundamental to meeting their changing needs. With our newly developed ESG Score, you can identify those customers who are most concerned about ESG issues. Download the product sheet to continue your ESG journey.

Data is key for successful businesses to take decisive action on sustainability

Sagar Limbu